Original Link: https://www.anandtech.com/show/2364

The Business of Technology: Intel Q3 2007

by Ryan Smith on October 30, 2007 3:00 AM EST- Posted in

- Bulldozer

In our first Business of Technology article, we took a look at the audio industry's falling star, Creative Labs. As the first in a new series of articles we were especially interested in feedback from you, the reader, and were not disappointed. Thank you for that feedback, it hasn't fallen on deaf ears and has gone into improving this and future Business of Technology articles.

With that out of the way, for our second article in this series we'll jump right into the fray and take a look at one of the titans of the computer industry: Intel. Intel has a long and rich history; so long in fact that the company existed before most of the AnandTech staff, a bit of a rarity in the computer industry. It's the long history of Intel and the ramifications of such that make it such an interesting and unusual company to fully grasp.

While we take a look at a number of Intel products here at AnandTech, few people actually realize the scope of the company - from our reviews you would think that Intel is a processor company, a chipset company, a motherboard company, and that's it. In reality they're also a major player in wireless communications, graphics (albeit integrated), flash memory, networking, embedded chips, and more. Processors are their biggest source of revenue and profit by far, but the other groups nevertheless still play a part.

As is customary with this series, today we'll take a look at Intel from both sides - business and technology - to understand what the company has been doing the past quarter, and where they are going in the near future. Intel is of course a very powerful technology company, but they also do a solid job of managing their overall business interests. As we'll see, this has made Intel a very solid company over the past quarter, but also one that will be fighting against growth concerns.

Intel by the Numbers

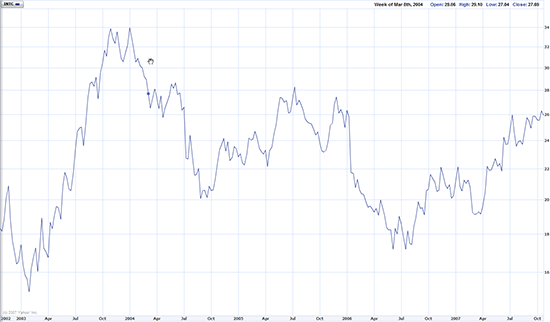

For our look at Intel's business side, we'll start with the barometer of the overall company status, the stock price.

5 year stock history, courtesy of Yahoo! Finance

The stock market can be a very fickle beast, and not for reasons that immediately make themselves obvious. Depending on how far you want to go back in looking at their stock, you get two very different pictures. In the past year the stock has picked up over four points, for an increase of almost 22%, but if we go back a full 5 years Intel is effectively flat at best. In either case the stock is well above its lows of either period, but in the 5 year span specifically, it's well below its highs and is currently in a point that is effectively flat.

Intel's stock is further notable in that it is a dividend stock (a stock that returns regular dividends from profits) when many technology companies don't pay a dividend at all, rather opting to put all of their profits back into the company. This tempers the movement of the stock some, as investors will buy it with expectations of profiting from dividends and share price growth, rather than solely share price growth. This also means however that for better or worse, dividends are already factored into a stock price and that dividend growth is a required component of stock growth. Intel only pays out a very small fraction of its profits as dividends (on the order of less than a percent per quarter) but they are still not immune from the expectations created by dividends.

Dividends of course are a direct result of profits and revenue from the quarter, which is what we'll look at next.

The primary reason we can call Intel a strong company is its revenues and profits. Intel hasn't been in the red for over a decade - even in particularly bad periods such as the post-dot-com bubble burst and their more recent troubles with the underperforming NetBurst architecture, the company has continued to record a profit. Thanks in a large part to their dominant position in the processor industry, they're one of the few technology companies that can claim such a long streak of profitability.

So with the revenue and profit in mind, why is their 5 year stock performance so poor? In a word: growth. There is a lot of concern in the investment community that Intel has completely tapped most of the market for computers globally. Although the computer is still nowhere near 100% saturation even in the most affluent nations like the television has become, there are few remaining groups that would be first-time computer buyers. Current computer owners have already settled into an upgrade cycle, but they're not likely to spend more on their next computer than their previous (adjusted for inflation where appropriate). For the stock to grow the company needs to grow; for the company to grow they either need their current consumers to consume more, or better yet find new consumers.

To get an idea of that situation, we have the basic product revenue breakdown from Intel's financial reports.

| Revenue By Business Group (In Millions) | |||

| Q3 2007 | Q3 2006 | Q3 2005 | |

| Digital Enterprise | 5204 | 4946 | 6370 |

| Mobility | 3971 | 3048 | 2970 |

| Flash Memory | 553 | 507 | 573 |

| All Others | 362 | 238 | 47 |

| . | |||

Unfortunately Intel reports this breakdown in terms of their business groups, which are not the same as their product groups. The processor revenue for example is split between the Digital Enterprise Group (PCs and servers), the Mobility Group (laptops and handhelds), and the much smaller Digital Home Group (set-top boxes and consumer electronics). But we do know what portion of the first two groups in particular are processor sales, which gives us an overall idea of what their processor revenue is like, and how it compares to the whole.

With the formation of their business groups in 2005, we only have just short of 3 years of comparable breakdown data, but there is a clear pattern in looking at it that much like Intel's stock price, their processor revenue is effectively flat, neither surpassing their highs or scraping their lows. This is in spite of their current technological advantage (more on that later) and has much to do with AMD. Intel's processor and chipset revenue is such a large part of the company that it effectively dictates the overall condition of the company financials, and right now Intel is still being held in check by AMD in some respects.

As we've touched on in our previous articles, AMD can't compete with Intel in the high end PC market with their current K8 architecture, but this hasn't stopped AMD from doing so in the low-end and server markets where they are stronger. Here AMD is fighting with pricing, cutting off Intel's avenues of growth through higher prices. The flat processor prices that result from this are the main thing being blamed for Intel's limited revenue growth. For this quarter in particular, it's an increase in total processor sales that buoyed Intel and helped them come in over analysts' expectations.

In response to the pricing pressures, and on the eve of AMD's Phenom launch, Intel seems prepared to play the pricing game for a protracted period of time. Intel has been shedding employees at a steady rate so far this year and will be continuing to do so for the rest of the year. The company started 2007 at 94,000 employees, and at this point is expecting to end it with 86,000. With the inability to control the pricing of the processor market, Intel has cited this as one of their key efforts to maintain and grow profits, by reducing overall costs and boosting the profit on each processor.

Finally, as Intel does from time to time, they're jettisoning a low-profitable/non-profitable business operation. Intel has left a number of memory businesses over the years, and until now their last memory business has been NOR flash, a less common form of flash memory that is used for direct application execution on devices like cell phones, thanks to its full random access capabilities. The NOR flash business has been losing money for some time now, and Intel has finally decided to cut their losses and spin off that business in a joint venture, mirroring what they did with their NAND business a couple of years ago. Intel's losses in flash memory so far this year have been particularly brutal (nearly three-quarters of a billion dollars), so this will further boost company profits, at a decent hit to lost revenue.

Going into the fourth quarter, Intel will also be doing so a further $150 million out of $250 million lighter, thanks to a settlement they've reached with ailing processor designer Transmeta over patent issues. The $150 million initial payment isn't a significant loss for Intel (it would be about 10% of their profits for Q4 2006), but it will temper most chances of a spectacular quarter.

Intel's Technology and Closing Thoughts

In comparison to Intel's business situation, their technology situation is fairly straightforward, both in the present and near future thanks in large part to their detailed plans released at the twice-yearly Intel Developers Forum. Rather than repeat what we've said before, we'll provide a quick recap on Intel's technology and product situation. For a more complete description these matters, please take a look at our Fall 2007 IDF Coverage.

On the desktop and mobile markets, Q3 and the rest of 2007 have been very good to Intel. With AMD unable to compete with Intel at the high-end, Intel has the superior technology and has been able to enjoy the higher margins that the high-end provides. At the midrange and below where AMD can compete in performance, their price competition has prevented Intel from being able to clench the same kind of dominating position, but even this is not a bad situation for Intel; it's merely less than ideal. Even with price parity, holding the high-end offers the winner the chance to capture a disproportionate amount of mind share among all prices, which further improves their share of actual sales in the competitive price rangers.

Now in Q4, Intel is about to begin the "tock" phase of their "tick-tock" product release schedule with the release of their 45nm Conroe-derived Penryn parts. With the initial reports of these 45nm parts being very favorable, and AMD not expected to be able to immediately compete with Intel on the high-end with the Phenom launch this quarter, Intel's technology situation in Q4 will largely be the same as that of Q3. Because only a fraction of their CPUs shipped in Q4 will be on the 45nm process, any significant impact from this launch is still a couple of quarters away. The highlight of the situation for Intel will be the usual seasonal pickup in sales, along with the additional bonus of power users upgrading to the new 45nm products.

On the server side, things are and will continue to be less certain for Intel. They're still well in the lead by total volume, but AMD has nonetheless managed to stay competitive with Intel across the entire x86 server segment. Intel's current 45nm schedule for servers is fairly aggressive, giving Intel a leg up against the recently launched Barcelona. However the Xeon line continues to suffer performance and power usage handicaps due to the limitations of their FSB and the use of FB-DIMMs respectively, and Barcelona doesn't need to deal with either of these. With no clear winner across the entire server spectrum, our best assumption is that Q4 will go much like Q3, however with Intel standing to lose some market share. The bigger shifts will be next year.

The press-neglected Itanium line will also be seeing a slight update in Q4. Intel will be releasing a minor refresh of the Montecito, the Montvale, which will bring slightly higher FSB and core speeds along with some new power saving technology. Because Intel does not manufacture the Itanium line so close to the bleeding edge of their process technology, Montvale will still be a 90nm part like Montecito. The Itanium line won't be moving to 65nm until late in 2008.

Finally, the rest of Intel's major product lines will be fairly quiet for Q4. Q3 saw the release of most of the Bearlake series of chipsets for desktop machines, and Q4 is seeing the slow release of the X38 (with X48 now a 2008 part). Also, Intel's software division made a particularly interesting acquisition in Q3 with the purchase of physics and animation middleware provider Havok. Intel hasn't been clear on the reasons for this acquisition, but it's safe to assume that this is driven by Intel's desire to speed along the poky advancement of physics software that effectively uses multiple processor cores, as improvements in per-core processor performance will continue to stagnate compared to the growth in the number of cores per CPU.

Closing Thoughts

Earlier we called Intel a strong company, but we also called them a company that has to fight growth concerns. There is no question in our minds that Intel is currently at the top of its technology game; even in their weakest market (servers) they're still doing very well, while enjoying complete performance dominance of the desktop and mobile markets. On the other hand, Intel's business side is struggling to appease the investment community, in a situation that at first glance is quite odd.

Intel's problem isn't its technology, nor is it an exciting business problem such as bad investments or marketing - the problem is revenue growth. A company holding stagnant is a company one step away from shrinking, which is why there's an expectation on Wall Street that a company should always be growing, and growing as fast as it reasonably can. The issue is that Intel has reached consumer saturation; there just aren't many people left to sell processors to that don't have one.

In the long term Intel will be solving this with new products such as cheaper processors for poorer markets, but Wall Street is looking at the next quarter, not the next year. In lieu of growing the customer base, the short term solution is to grow the profit margins on their products. This is part of the reason why the new 45nm chips will initially be allocated to high-profit, high-cost fields such as servers and the Extreme Edition line of processors, where both markets will pay a significant premium on a processor. It's an unfortunate situation, but isn't something that can be helped. Sometimes the realities of business get in the way of the advancement of technology; this is one such case.

Let's not get too depressed in what is a fairly minor detail that only matters for a handful of people, compared to the rest of the picture. Coming out of Q3 and into Q4, Intel is in the position of a strong company with market dominating technology, and a well developed business practice that keeps the company very profitable. They'll certainly be continuing that trend for the rest of Q4, and into 2008. What about their main competition? Stick around, we'll have our look at AMD's Q3 later this week.