Original Link: https://www.anandtech.com/show/2368

The Business of Technology: AMD Q3 2007

by Ryan Smith on November 2, 2007 1:00 PM EST- Posted in

- Bulldozer

In the first part of our Business of Technology double-header, we took at look at Intel, who had a great 3rd quarter, but is navigating concerns of slowing growth. For the second part of our look at the CPU titans, we'll take a look at AMD, a company who isn't sharing in such a rosy financial outlook.

AMD is very much the yang to Intel's yin (or the other way around if you prefer), being the other major producers of x86 processors and the only other producer to actively target the high-end. Furthermore with the acquisition of ATI last year, AMD is now also NVIDIA's counterbalance. This puts AMD in interesting and critical position of keeping both of the big players in check, a difficult task at times.

AMD is in some ways still a company trying to grow in to its place in the market. We have reviewed their products for as long as they have existed, but on the CPU side specifically, for all practical purposes they're not on the same level of an old, established player like Intel is. AMD has produced CPUs for a over 30 years, but the first 19 of those years were as an Intel clone manufacturer. 1996 saw the release of their first in-house design, the K5, unfortunately it and its successor the K6 both underperformed compared to the best Intel chips of the time.

If we want to talk about AMD as a completely competitive force in the x86 market, we're looking at a scant 8 years; it wasn't until the K7 in 1999 that AMD produced a chip that could beat Intel in performance on the desktop. It wasn't until even later, 2003, that AMD finally made a meaningful break in to the server market, finally cementing their place as Intel's peer in the x86 market.

In their limited years as Intel's peer, AMD has done some amazing things, but they have also had to learn how to operate a business like a major player, something that has been difficult for them. Intel has lost money only on a handful of years, a good year for AMD since their emergence as a true x86 competitor has simply been to not lose too much money. AMD is still a raw business, sometimes for the better, other times for the worst. Yet we can't understate just how important they've been for the x86 industry.

Today we'll take a look at the business and technology aspects of AMD for Q3 2007. Q3, like the rest of 2007 has been extremely painful for AMD; we'll dive in to what's going on that has caused so much pain for what may be the most important GPU/CPU manufacturer on the competitive market, and what AMD is doing over the next quarter to reverse their fortune.

AMD By The Numbers

As always, we'll start this Business of Technology article with a look at AMD's stock price, a solid gauge of their overall health.

5 year stock history, courtesy of Yahoo! Finance

In spite of AMD's current situation, the stock has still done worse over the 5 year period, something not hard to imagine given the company's status of often hanging on by a thread. Their stock is still up almost three-fold compared to their lowest point prior to the launch of the K8. Going by their stock alone, AMD would appear to still have some breathing room should the fall further.

However as K8 sales set up AMD for a period of strong business growth and high stock prices, it has also set very high expectations for AMD that they have not been able to meet. The stock has fallen nearly 75% since its 5 year peak, and nearly 50% in the last year. The price drop represents both a dissatisfaction from Wall Street on AMD's future outlook, and a punishment for losing so much money over the last year.

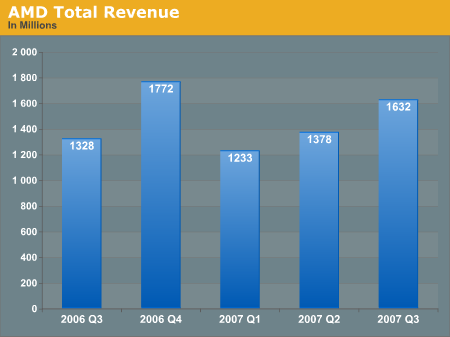

How much has AMD lost, and how does that compare to their total revenue?

Because AMD acquired ATI in Q4 2006, we do not have completely comparable data for Q3 of 2006. The change in revenue between the two Q3s as a result is not solely revenue growth, but is rather a combination of that and the addition of ATI's products to AMD's business.

All told, the total revenue situation is actually good for AMD. In spite of the fierce competition with Intel and NVIDIA, their total revenue after removing their graphics revenue is still up a bit. Furthermore in this quarter they managed to beat Wall Street's rather pessimistic projections for revenue, thanks to overall processor sales that were above those expectations. AMD's price war with Intel has allowed them to keep their chips selling well (prices aside) while the Barcelona launch in September further boosted revenue.

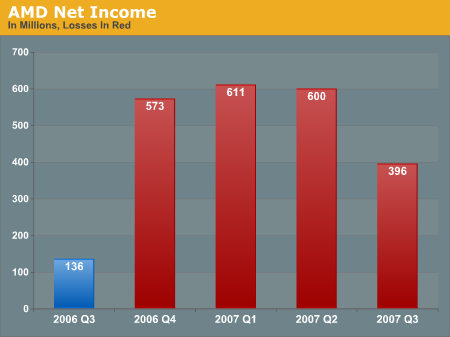

Profits are less rosy however. The higher revenue has offset what was expected to be worse losses in Q3, but it wasn't nearly enough to move AMD close to profitability. Since their dip began, AMD has lost over 2 billion dollars on revenues of 6 billion; or in other words spending about $4 for every $3 of revenue. It's sufficient to say that this isn't something AMD can keep up, but for now their losses are lessoning.

So what have they been losing so much money on? Contrary to popular belief, this isn't solely due to price wars with Intel and NVIDIA, which is very good news for the company. We'll take a look at the segment breakdown to explain why this is.

| Revenue/Net Income By Business Group (In Millions, Losses In Brackets) | ||||

| Q3 2007 | Q2 2007 | Q1 2007 | Q4 2006 | |

| Computing | 1283/(112) | 1098/(258) | 918/(321) | 1486/65 |

| Graphics | 252/(3) | 195/(50) | 197/(35) | 166/(27) |

| Consumer Electronics | 97/(3) | 85/(22) | 118/(4) | 120/20 |

| All Other | 0/(108) | 0/(127) | 0/(144) | 1/(587) |

| . | ||||

Overall AMD is losing money on all of its major businesses, but their consumer electronics and graphics divisions are losing comparatively little money (so little in fact that they may as well be break-even), it's the processor and "other" segments that are the real money losers. For the processor segment in particular, AMD is not losing any money directly from chip manufacturing in spite of the price war, it's only after additional costs such as R&D are factored in that the segment is losing money.

The segment eventually needs to pay for its R&D, but to be losing money now, on the eve of the rest of the K10 launch, isn't a bad place to be. Furthermore AMD has managed to improve its gross margin (the percentage of revenue after the cost of goods) on its product range from a particularly low 33% to a stronger 41% between Q2 and Q3. A low gross margin had been an important factor in contributing to the processor segment's losses, so improving it is the biggest step to digging that segment out of the red.

Next, when we take a look at the "other" segment we can begin to understand where AMD is really losing much of its money. "Other" isn't a segment of real products, but rather the segment where AMD categorizes all expenses that don't fall in to other segments; this includes acquisition expenses, stock compensation expenses, and profit sharing. As it turns out, most of the $108 million that was lost was due to the ATI acquisition, which AMD is still paying for. The costs of the acquisition have set AMD back by $256 million so far this year. But (and this is the good news) these costs will be coming to an end soon. The ATI acquisition hasn't been the only thing pulling AMD down, but it's also a temporary cost that will be coming to an end on its own.

There is one final money pit for AMD however that can't be buoyed up by any good news at the moment, and that's debt. AMD has never been in a position or a desire to be completely debt-free, but right now they're swimming in it. AMD needed to borrow money in the first place to be able to buy ATI, but this has been further compounded by their losses. AMD spent nearly $100 million just on interest charges in Q3, and this has been growing steadily since they started posting their latest series of losses.

To give you an idea of what kind of debt AMD is in, we have the assets & liability numbers from both Q3 2006 and Q3 2007. In Q3 2006, AMD held nearly $8.4 billion in total assets and held $689 million in actual debt among $3.4 billion in total liabilities. In Q3 2007 they held nearly $13 billion in total assets (mostly from the ATI acquisition) but held $8.8 billion in total liabilities, $5.3 billion of which is debt. The fact of the matter is that between absorbing ATI's debt and adding to their own, AMD has racked up nearly $5 billion in debt in the last year. It goes without saying that this is very, very bad.

In closing on the subject of business, there has been a lot of concern if AMD can stay solvent for much longer. Looking at the numbers, rumors of AMD's impending death are a bit exaggerated. Barring any outside influences such as their own acquisition, AMD still has time left, but that time depends on what their losses are like. If AMD curbs their losses (and we expect this to be the case as things like the ATI acquisition come to an end) we're looking at a lot of time - AMD will be sound well in to release of the Bulldozer core in the future. But if they really want to turn things around they need to bring their processor and graphics segments to profitability, which as we'll see in our discussion on their technology, is a tall order that can be filled, but will be a challenge to do so.

In the mean time we can't ignore the effect that the ATI acquisition has had on AMD. It's not the cause of all of their woes, but it is the cause of a lot of them. We hope for AMD's sake that they're right about the GPU and CPU merging, because this entire endeavor will have been a significant drain on the company if Fusion and its derivatives don't pan out like AMD wants them to.

AMD's Technology & Closing Thoughts

Because of the nature AMD's poor financial situation, the key to the company's recovery must lie in its technology. In the processor market, AMD's position as a provider of low-cost, mass market CPUs is unsustainable given the costs of R&D for future processors, so they need to make the kind of technological advances that will launch them back to the top. Their graphics operation is under a similar premise, although their position there is not nearly as far behind the market leader.

We'll start with AMD's best strength right now: servers. 4 years ago AMD made a very, very good choice in creating and using HyperTransport, as this has scaled much better with 4P and higher systems than the traditional front side bus has. AMD's choice to use an integrated memory controller and NUMA has also worked out very well, as they can use large banks of traditional DDR2 DRAM instead of needing to use FB-DIMMs to achieve such large banks.

Both of these choices have enabled AMD to be very competitive with Intel in the server market, which is great news for the company as server processors (especially 4P and higher) are products with high margins that can be funneled back in to R&D and other projects. At this point AMD can't claim the best server performance scores across the board, as the Intel's Core 2-derrived Xeon chips can muster more overall performance, but the situation is such that the Xeon is being hobbled by the FSB and FB-DIMMs, which increases AMD's relative competitiveness. Furthermore, even with their older K8 processors AMD has been able to offer very good performance the performance-per-watt category, a metric of particular importance to datacenter operators who are using blade-style servers and other setups where there are practical limits on how much heat can be dissipated.

Q3 saw the launch of the Barcelona design, a particularly important change for AMD. They can now offer chips that have better overall performance than their old chips, and they have a quad core design to compete with the quad core chips Intel has been offering for some time now. This has closed some of the gap that has formed over the last year as Intel outpaced AMD, and as a result Q4 is going to be a big quarter for AMD as it will be the first full quarter with the Barcelona shipping. Unfortunately Barcelona isn't a new Intel killer, at current clockspeeds it's still underperforming Intel's best chips, and we don't know how much that is going to change.

Intel has the 45nm advantage, meanwhile AMD was unable to get a suitable amount of 65nm K8 chips to clock as high as the older 90nm K8s, so we're a bit concerned on just how good AMD's 65nm process is. This doesn't preclude the possibility that K8 scaling problems were due to design issues and not process issues, but AMD has never released enough information one way or another that we can put our worries to rest. For now AMD is in a respectable position, they can't offer the best server performance, but it's good enough for the current market. And while it's entirely plausible that their server division could do very well in the long term even if they were always behind Intel by a small amount, it's not an idea that is a good one to test. Simply put: AMD needs to raise its clockspeeds enough to completely compete with Intel if they want a guaranteed recovery in the server markets. For Q4 at least this isn't going to happen, and we're going to be looking at 2008.

Moving on to consumer processors, it's virtually the same story. The first numbers for Intel's latest high-end 45nm Penryn parts is very good, meanwhile we aren't expecting AMD to be able to match those parts with the Phenom line this year. Much like Barcelona, Phenom is still an important launch because it closes the gap, but AMD doesn't have other technological advantages here like they do in servers to offset this gap. Right now the Phenom launch won't push the company back in to profitable territory, but it will enable AMD to raise their average sales prices and cut some of the loss. Phenom's effect on AMD's situation will be much greater once it has shipped for a full quarter in 2008. Q4 however is seeing the first full quarter of AMD manufacturing at 65nm exclusively which is helpful for margins. With the shutdown of Fab 30 AMD no longer has any 90nm production facilities (although partner Charter may still be able to produce 90nm parts).

As for the graphics side of AMD's business, how Q4 will go may as well be anyone's guess. We know AMD will be launching a new line of GPUs this quarter, but we don't know how many, or with what kind of performance. In total performance the X2900XT was not enough to beat the GeForce 8800GTX, which deprived AMD the chance to sell extremely high-margin parts. The GPU industry, more so than even the CPU industry, is heavily biased in sales at the low end, so AMD was fortunate in that they missed out on comparatively few high end sales. This is a market where it's entirely possible to focus on volume sales and reach profitability, without the need to compete at the very high end of the performance spectrum. AMD's graphics division was after all almost profitable for the quarter, so no significant changes are required to reach at least some level of profitability.

But in the future AMD risks falling in to a trap similar to the R&D costs trap of the CPU industry if they aren't developing the high-end technology that will filter down in to lower products. With that said much of this rides on what their next generation of GPUs can do. We have no reason to expect AMD to be comparatively any worse off than they were with the Radeon HD2900XT, so what we're really looking as is if they can improve and by how much. A GeForce 8800GT killer is a must, so we're looking forward to seeing such a product hit the market.

We are slightly concerned however that they haven't made a particularly strong effort to push the GPGPU aspects of their GPUs. Like server CPUs, GPUs in a high performance computing GPGPU environment can fetch high margins, and rival NVIDIA has made a very focused effort to capture this market. We'll have more on this issue specifically in a future article, but for now it's an oddity that AMD hasn't taken better advantage of this market.

Wrapping things up, this quarter will see the launch of the first of AMD's new 700 series chipsets to coincide with the Phenom launch. Chipsets are a great revenue source to go with CPU sales, so it's to AMD's advantage here to pair up more of their chipsets with their processors, instead of letting NVIDIA have such a big piece of that market. AMD's embedded division will be seeing a lot of fanfare with the first major Geode-using OLPC shipment going out this year, but as the OLPC is strictly a non-profit venture this won't immediately help their situation. However it could spur for-profit sales, which would be a good thing for the company.

Closing Thoughts

We won't attempt to sugarcoat AMD's Q3 and say it was any kind of recovery quarter; it was simply the latest in a string of bad quarters for the company. AMD is in a price war with Intel it is so far winning, but is costing the company too much right now. Furthermore the acquisition of ATI has proven to be very costly, and the direct costs of the acquisition and the borrowing for it are not treating AMD well. They can't have too many more of these quarters, and while things are going to get better on the business side as loans and other costs are repaid, Q4 will more than likely also be a losing quarter for AMD.

The best AMD can hope for in the rest of Q4 is cutting their losses, and this is something that is going to be executed through their technology. The Barcelona Opterons and the new Phenom processors can't reverse the company's fortunes in this quarter, but they are closing the gap with Intel, raising AMD's margins, and breaking the cycle of the painful price war AMD has been in. AMD will always be at some technological disadvantage compared to Intel due to Intel's better manufacturing process technology, which means AMD needs to be all the smarter with the advantages they do have, and Q4 will be about using those advantages. Meanwhile depending on what AMD releases for GPUs this quarter, their graphics division may finally start turning a profit for AMD, further absorbing AMD's other losses.

It's admittedly painful to see AMD in their currently situation. As consumers, things are best for us when both AMD and Intel (and AMD and NVIDIA) are at each others throats, and this isn't the case right now. AMD isn't going anywhere yet, but AMD needs to be at Intel's throat soon if they ever want to do it again.